Fixed Income Review - October

- Soham Mukherjee

- Nov 17, 2018

- 3 min read

Treasury Yields Push to the Upside, Cryptos and Rare Commodities Rally

Treasuries, which all investors hail as the definitive risk-free rate of return when evaluating financial assets, once again made a big impact on markets in October. The U.S. 10-year note’s yield broke through and finally cleared the 3% mark which had been a key level of resistance for the past 8 months.

With this rise, investors again began to worry about rates becoming more attractive which could lead to a broad equity market decline. Couple that with fear of these higher rates slowing economic growth heading into the third quarter earnings season, we wound up with the biggest S&P 500 drop since 2011.

What was more interesting to note was that during this sell-off investors made a big push to Bitcoin and gold. Historically, gold has rallied during periods of uncertainty, but the emergence of cryptos has created a new “safe haven” for people to store their money.

The Fed: Should Trump Be Barking? Absolutely Not

The Federal Reserve Bank was formed in 1913 as an independent entity of the United States Federal Government. The only authority the government has over the Fed is who is elected as its chairman which took place this year with President Donald Trump’s appointment of Jerome Powell. Outside of that, the Fed is designed to be an independent entity that should remain uninfluenced by political forces while conducting monetary policy (the Federal Government is already in control of fiscal policy).

While that has been the case for the most recent prior administrations, President Trump has again endeavored on an unprecedented accord by attacking Jerome Powell’s decision to increase the federal funds rate yet again in the wake of an accelerating economy.

Trump called Powell’s move crazy, claiming that raising interest rates to quickly would cause the economy to rapidly sputter into a recession, eliminating all the gains from his Tax Cuts and Jobs Act which passed in the final days of 2017.

For Trump, the economy has been the high point for his supporters. GDP grew 3.5% in Q3 2018 which has helped keep his base strong, but Trump recognizes that he needs to hold up until at least 2020 to get re-elected. With these political motives, the question becomes a bit easier to answer: no, absolutely not; he shouldn’t be commenting for his own political agenda.

The Federal Reserve maintains its integrity by making decisions that the chairperson and board believe is in the best interest of the U.S. economy. Its job is to serve the best financial interests of American people and institutions, not to help support political agendas. While President Trump’s concerns may or may not be legitimate, it is best for the American people if there remains an independent separation of power.

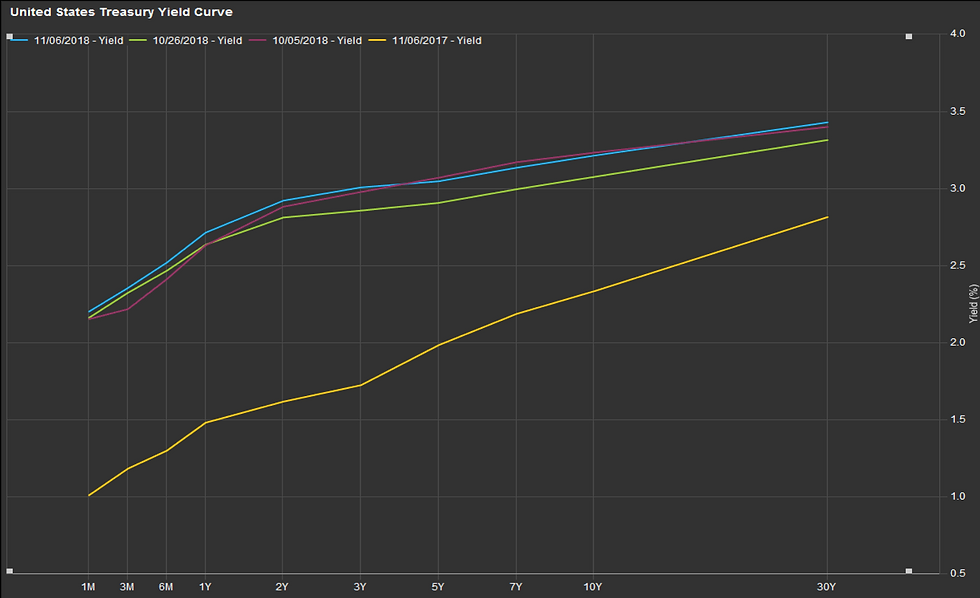

Yield Curve Analysis

Over the past few months, yields have risen as the Fed appears to be hawkish in the face of a thriving economy where inflation is expected. This inflation has become a stronger looming figure as wage growth has picked up for the first time in decades, rising 3.14% this past month. This coupled with the feds statement saying “neutral rate is still several hikes away” indicated they plan to raise rates further this cycle.

This rising by the Fed has been further exacerbated by the current administration's tax cuts which have required the government to finance more of its activities through debt, increasing the issuance of treasuries. This influenced on investor sentiment can be seen in the quick increase in bond yields as well as the flattening of yields. As we can see from the chart above this sentiment briefly retreated throughout October before picking up again this past week surpassing the previous month’s flatness. This flattening indicates several things.

First, a flattening curve shows that investors are requiring less compensation for their term premium relative to the short end of the curve. This shows that investors are not worried about inflation eating away returns meaning they believe business will not be able to raise prices. This happens when an economy slows down. In part, this slowdown is usually attributed to the increased rates which have two effects. The first is higher rates incentivize households to invest rather than spend money, slowing consumption which is the main driver of the US economy. Secondly, they make borrowing more expensive as well which deters companies from expanding operations which is how hiring occurs. This means that this flattening is a precursor to an economic slowdown.

These climbing yields also decrease the price of current outstanding bonds as prices must fall to match the yield of other comparable bond offerings. This makes rising rate environments an uphill battle for bond funds as few, if any, hold positions until maturity.

Comments