Derivatives - April 2018

- Soham Mukherjee

- May 6, 2018

- 9 min read

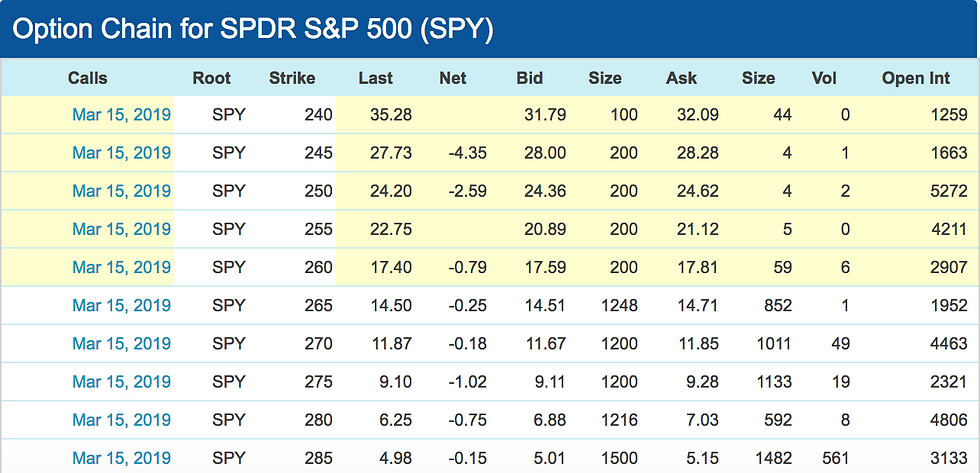

1) Data for SPY Call Options on May 3, 2018:

Below is data one can find on nasdaq.com for call options on the SPDR S&P 500. The data was taken on Thursday May 3rd, 2018. The options expire on March 15th, 2019.

Interpreting the Data Above the table in large numbers is the current price of the asset. The rightmost column tells when the option expires, which is less than a year from now on March 15th, 2019. The strike price represents for what amount of money the holder of the option has the opportunity to buy the asset. For example, a strike price of 270 is equivalent to saying “You have the right to buy the SPY for $270, regardless of its underlying price, at any time until the expiration date”. However you only have this opportunity to exercise once during the period.

“Last” refers to the most recently traded price that has been posted. Net refers to the change in last compared to the previous trading day’s end. A negative value of net means that the option is trading for less than it was the day before; seeing that the underlying also decreased shows that the two often work in tandem. The Bid and Ask represent the prices at which buyers and sellers are respectively willing to buy and sell the option.

Buyers will tend to demand a lower price while sellers will try to gain greater compensation; the transaction price will often fall between the two values. The size of the bid ask spread can indicate an option’s liquidity: the smaller the spread the more liquid the option; the opposite holds for larger spreads. Volume shows the number of options transacted at that strike price during that trading day, and open interest captures all of the total positions on a particular strike price that have yet to be closed.

An important feature not directly stated on an option chain is that when you purchase a call option on the SPY, you are actually given the option to buy 100 shares.

Thus to derive the total cost of a single purchase, you must multiply the costs by $100. For example, at the $270 strike price an investor would have to pay 11.87*100= $1187 for the option to buy 100 shares at $270 each. Now let’s suppose the price of the SPY increases to $290. The investor would exercise his option and buy shares at $270, generating a total purchase of 270*100= $27,000. However because the current price is above the underlying, he would immediately sell his 100 shares at the market price of $290 and pocket a 290-270=20*100=$2,000 profit.

Let’s compare how the returns would differ if the investor had bought the stock as opposed to the call option. If the investor had bought the stock at its currently underlying price of $262.62, he would have made approximately a 10.4% return. However with the option, the investor would have achieved a 68.5% return due to the fact that she only had to put up $11.87 as opposed to $262.62.

Despite the magnified returns, it would be a mistake to think options always offer more consistent profits. Let’s suppose in the previous example, the stock reached $269. It is still an increase from the initial underlying, but because your stock option has a strike price of $270, your option will expire worthless and you would lose all of your initial investment. In fact, to just break even, the SPY would have to increase to a price equal to the strike price plus the cost of the option.

In our example that would require the price to reach nearly $282 before any profit is made. In both of these events, simply buying the stock would have yielded a positive and respectable profit. One last advantage of the option is the lower bound on the amount of money the investor could lose, which is equal to the price of the option. If the SPY were to collapse down to 200, the stockholder would suffer great losses, but the option holder, although subject to significant percentage losses, would only lose the capital equal to the amount paid for the option.

Why do call prices vary?

Looking at the option chain, it is evident that the price of a call option decreases as the strike price increases. This makes sense as the higher the strike price, the less likely it is that the stock will reach that threshold. In the event that the relationship does not hold, such that a call option with a higher strike price costs more than a call option with a lower strike price, an arbitrage opportunity would exist.

Investors would sell the higher priced call option and buy the lower priced option; the increased demand for the lower strike option would increase its price and the decreased demand/increased supply of the higher strike option would decrease its price until it is lower than lower strike option.

The amount of time until the option expires also determines the price of an option. As the time to expiration increases, the price of an option will also increase. This should make intuitive sense, as the option has more time to break through the strike price. The table below shows call options expiring on August 17, 2018 (see the fourth column for prices). Because there is less time until the expiration date, the prices seen are lower than those above.

Volatility is another factor that will impact the price of an option. All else equal, the more volatile a stock is, the more expensive its call option will be. The underlying asset much surpass the strike price to generate returns, and more volatile stocks will have a greater probability of breaking that barrier than non volatile stocks. If you imagine a stock’s gains or losses as a series of jumps, then to become profitable, a very volatile stock would only need a couple bounces in the right direction, whereas a less volatile stock would need many incremental bounces to find itself with a positive payoff.

If a stock becomes more volatile during the life of the option, it will have higher expected price fluctuations and thus will become more expensive. From the viewpoint of the seller of a call option, volatile stocks could potentially put you in a large hole if their volatility works to the upside, so to compensate for this risk the seller would want to charge a greater premium for the option. If market volatility decreases as a result of muted inflation, call options may dip in value.

If the opposite holds and higher inflation readings prompt the Federal Reserve to accelerate interest rate increases, volatility may jump and take call options prices along with it.

How should I invest in a SPY Call?

There are many ways an investor could trade call options, and ultimately it depends on his outlook on the market. The method we have outlined thus far has involved the investor purchasing a call option and then waiting until the expiration date to determine the overall payoff. It is definitely possible to execute that plan, but savvier investors will look to craft more complicated ways to gain profits in quicker manners.

One simple way an investor could make a profit through options is by selling the option before it reaches its expiration date. The price of the option depends on many variables, but let’s assume the simple case where the underlying price increases up to 267 from 262 by the end of May. The call option with strike price of 270 that the investor holds should now be worth more than $11.87. This should hold true because the underlying price has increased such that it is much closer to the strike price, and there is still a respectable amount of time until the expiration date.

If the price of the option is now $13, the investor can go out into the market and sell it to pocket a profit of $1.13, which is multiplied to become $113. It is important that the option is liquid, so the holder can easily find a buyer to complete the transaction. An investor may want to sell the option before expiration date if they are risk averse and are content with a modest profit. An investor can both buy and sell call options to develop different positions. If the investor believes that the market is going to increase, but only modestly, they can take a position known as a call spread. This would involve buying a call option at a lower strike price and selling one at a higher price. Thus while the underlying trades at values between the two strike prices, the payoff will increase for one of the options that is in the money whereas the other is out of the money.

However once the price of the underlying exceeds that of the higher strike price, the obligation to pay on the higher option will cancel out the gains of the lower option, resulting in a zero net gain. An example of a call spread on the SPY would be to buy the 270 call and sell the 280 call. The investor would gain $6.25 from the sale of the 280 call, and pay $11.87 for the 270 call. The initial net payout of $5.62 translates to the fact that the underlying must only increase to $275.62 before the investor breaks even.

Call spreads put a ceiling on the total gains the investor can achieve, but it also lessens the total maximum loss, which is now the difference between the price paid for the option and the price gained on the sale. If you are an investor who believes that the market will increase over the next year, but that trade tensions, interest rate hikes, and inflation may mute those gains, then a call spread may be an appropriate investment. If you wanted to bet against the stock market, you could sell a call. To do so without also purchasing the underlying is known as a naked call, which is considered one of the riskiest positions to take as an options trader.

To sell a call gives you an initial cash flow, but also leaves you vulnerable to potentially infinite losses in the event that the underlying price increases. If the the call is exercise against you, you must go into the market and buy the underlying for its current market price, and then immediately sell it to the other party for the strike price. If the market price is much greater than the strike price, the naked call becomes a problematic investment. Naked calls would be an appropriate investment for investors who are very risk tolerant and hold a very strong conviction that the market is either going to decline in the foreseeable future or resist a rally over the next year.

For example, let’s suppose you sell a call at a 270 strike, giving you $11.87. The payoff would be the exact opposite as the one we examined for purchasing a call. Selling a call will ensure a profit as long as the price of the underlying is below the strike price plus the price of the option (approximately $282). Once the price exceeds the strike price of $270, your $11.87 will start to diminish until it is worth nothing at $282.87. If the underlying further increases to $300, you will find yourself with significant losses.

An easy way to mitigate the risk of a naked call is to buy the underlying at the same time you sell the call option. Thus in the event that the stock surges, you already own it and do not have to suffer the losses sustained in the naked call scenario. If you hold the stock, you do hold some downside risk as the stock could drop significantly and wipe out the premium gained from selling the call. If the stock increases such that it is lower than the strike price, you will make a profit on both investments since the call will go unexercised and the stock will have yielded a return.

A covered call is similar to a call spread in that the payoff has a ceiling (the stock and the sold call will cancel each other out once the break even value has been surpassed), but it also achieves a profit in the event of a small stock decline; as long as the call premium is greater than the magnitude of the stock’s decline. If you are an investor who believes that the market is going to maintain its current levels over next year, that the forces of increased earnings resulting from the new tax law and overall economic growth will cancel out geopolitical uncertainty and a rising interest rate environment, then a covered call would be an appropriate investment.

Conclusions

Options are great alternatives for investors who are looking to make great returns compared to buying stocks, as the amount of capital one must put up front is significantly lower while the payoffs follow essentially the same.

There are many factors that an investor must consider when choosing which call options they should purchase, and ultimately the optimal technique will result from their overall view of the financial and macroeconomic environment. Especially with the S&P 500, which serves as a proxy for the equity landscape, investors must develop well rounded opinions on overall market trends to maximize their positions.

Comments