Beta(r) Be Aware

- DFIG Writers

- Mar 27, 2018

- 3 min read

Updated: Apr 9, 2018

-Soham Mukherjee

Is abundant choice always a good thing ? Sure, if you are picking a restaurant to go out with your friends on a Friday night. Not quite if you are trying to calculate the beta of a stock to use in the Capital Asset Pricing Model when calculating the cost of equity which will finally be used in a Discounted Cash Flow (DCF) valuation of a company.

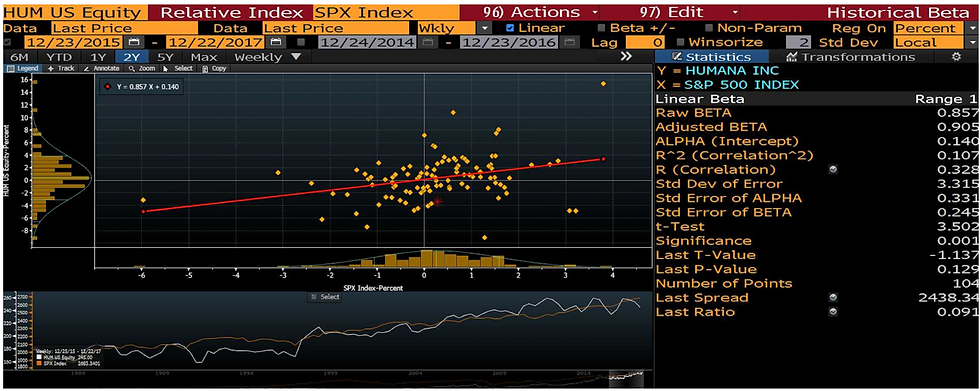

The above is a Bloomberg Beta Page for the American health insurance company, Humana (HUM). The danger lies here that Bloomberg gives me the ability to change the parameters on which the beta is ultimately calculated upon. I am able to change the “Relative Index” (which changes the index Humana stock is regressed against) or the “Data” (I can compute daily, monthly or quarterly returns) or how back I want to observe the stock ( 2 years to inception of the stock).

You give me a stock and ask me to find its Beta. I’ll ask you back “ Well, what do you want the Beta to be ?” Because I can use all the permutations and combinations and come up with that figure for you.

Yes, Bloomberg comes with default settings for all the above parameters but you know what this inbuilt flexibility can allow me to do right ? You give me a stock and ask me to find its Beta. I’ll ask you back “ Well, what do you want the Beta to be ?” Because I can use all the permutations and combinations and come up with that figure for you. You will then ask me “From where did you get it” and I will reply “Bloomberg”. That is is it. End of conversation. No further questions.

So I did just that for the Beta of Humana and here are some of my results from different combinations. Note that condition 1 is the default setting which Bloomberg provides me with.

As you can see, I only played around with it a little bit. But the results are already striking. The betas range from a low 0.276 to a high 0.952 and do not even get me started on the standard deviations which are all over the place and further skew the results. You can make a strong justification for each of the parameters used in the above cases. Of course, using the MSCI Emerging Markets Index (Humana is incorporated and conducts a majority of its business in USA) or the Russell 2000 index (Humana is classified as a large cap company) as the benchmark to calculate the beta will require you to be much more convincing.

To further drive home the capricious outcome this may lead to, let's use the above calculated betas in a Capital Asset Pricing Model to arrive at the cost of equity for the stock.

As you can see, I only played around with it a little bit. But the results are already striking. The betas range from a low 0.276 to a high 0.952 and do not even get me started on the standard deviations which are all over the place and further skew the results. You can make a strong justification for each of the parameters used in the above cases.Of course, using the MSCI Emerging Markets Index (Humana is incorporated and conducts a majority of its business in USA) or the Russell 2000 index (Humana is classified as a large cap company) as the benchmark to calculate the beta will require you to be much more convincing.

Hence, when I sit down to calculate the value of Humana to equity investors, I use my discounted cash flow method to calculate its unlevered free cash flow (or free cash flow to equity) and compute its present value using its cost of equity as the discount factor. But as you can see, the cost of equity can be so easily manipulated to give the company a value which you maybe required to produce at the offset.

So if I was an analyst and you were interested in buying Humana stock, I would use the discount rate of 4.03%, come up with a high value for the stock and make my case. On the flipside, if you were interested in selling Humana stock, well, I would use the discount rate of 7.28%, come up with a low value and make my case. You tell me what you want, I will get you the beta.

The bottom line is this. The beta reported by financial softwares is a purely statistical result which comes with standard errors, adjustments and easy manipulations. A better way of calculating the beta would be using a bottom up approach where you calculate an average beta of the various businesses that the company is involved in and take a weighted average of it, using sales or EBITDA (Earnings Before Interest Taxes Depreciation and Amortization) as weights.

Great article Soham!